European Central Bank Plans To Release CBDC By October, But Research Shows The Public Does Not Want One

However, the ECB admits many Europeans don’t want it, but claim they can propagandize the masses into accepting it.

European Central Bank (ECB) head Christine Lagarde recently revealed that the bank is eyeing to release its coveted digital euro, a central bank digital currency (CBDC), later this October. However, after making this announcement, the ECB admits that the public is still not on board.

The WinePress reported in October 2023 that the ECB had entered into a “preparation phase” with its CBDC development. Lagarde said at the time that “the digital euro is on the move,” making sure to note that “cash is here to stay.”

The ECB says that the digital euro is simply just a digitized form of cash, saying “it would offer another way to pay in stores or online shops, or to send money to friends and family.” The ECB adds, “a digital euro would be backed by the same institution that backs your cash – us, the European Central Bank. And just like cash, it would always be worth its face value.”

Lagarde said at the time:

“We need to prepare our currency for the future. We envisage a digital euro as a digital form of cash that can be used for all digital payments, free of charge, and that meets the highest privacy standards. It would coexist alongside physical cash, which will always be available, leaving no one behind.”

In an attempt to quash fears, the ECB published a report around that time to reassure Europeans that they have no intentions of mitigating their lives:

“With a digital euro, people would have more choice in how to pay and a secure solution that fully respects their privacy. The central bank has no interest in monitoring peoples’ payment patterns and no commercial aspirations. It would not have access to or store any personal data that would directly identify end users.

“The digital euro is also intended to achieve a cash-like level of privacy for offline payments, as it would require no third-party validation and would rely simply on the direct transfer from the payer to the payee.”

The ECB also acknowledged that in order for this to work, these new digital assets would not be stored on a digital ID wallet. “The Eurosystem would make available a digital euro app which would act as a uniform point of entry with a homogeneous look and feel for any end user to access digital euro services.” Furthermore, the ECB explains, “providing this app would ensure that basic functionalities are available, as identified by consumer’s associations and market surveys, as well as features supporting digital inclusion and the needs of people with disabilities and low digital skills.”

On cue, a month later the European Union voted on the creation of a new digital ID system. Commissioner Theiry Breton said, “Now, we have the digital identity wallet; we have to put something in it.” He presumably was referring to CBDCs and tokenized assets.

Fast forward to now - on March 6th, Lagarde revealed during a governing council press conference that the ECB is looking to unveil the digital euro this October. When asked about the status of the CBDC by a reporter, Lagarde stated:

“Nature does not like a vacuum. We started working on the digital euro way back, actually when I started my term 5 1/2 years ago. [We’ve] taken the lead together with a very good team, which is focused on accelerating the pace and hopefully campaigning enough with all the stakeholders – meaning the European Parliament, European Council, European Commission – so that we can eventually, not put to bed, but put to reality this digital euro.

“The deadline for us is going to be October 2025 and we are getting ready for that deadline. But we will not be able to move unless the other parties, the stakeholders as I call them – Commission, Council and Parliament – actually complete the legislative process, without which we will not be able to move. I think it is critically important, and for the agnostics or the sceptics, it now seems more relevant and more imperative than ever before, both on the wholesale and on the retail level.”

has warned of the dangers and problems introduced with a CBDC and tokenization, pointing out how the now-exiting Bank for International Settlements (BIS) - ‘the central bank of central banks’ - General Manager Agustín Carstens once ominously warned in a deleted video that a CBDC would provide “absolute control” over an individual’s life and purchasing habits.

But not to be outdone, Lagarde herself has even admitted that a digital Euro would remove anonymity.

Europeans Don’t Want It

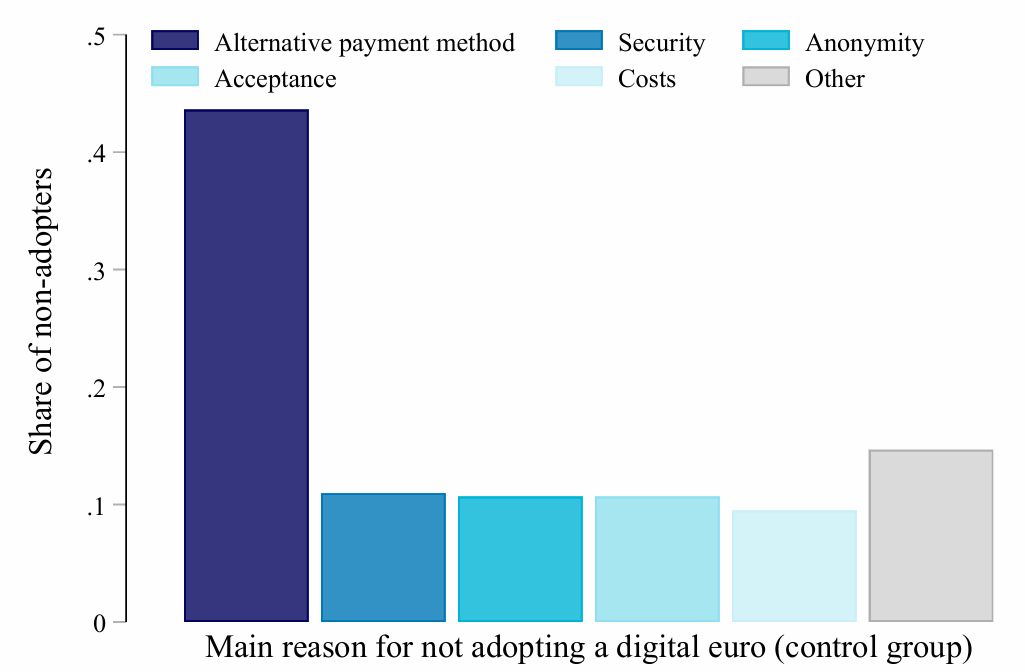

Since Lagarde’s latest announcement, the ECB has admitted that the majority of Europeans do not want a digital euro. Published last week, the ECB released a paper called “Consumer Attitudes Towards a Central Bank Digital Currency.” The paper cites roughly 19,000 respondents across 11 countries, which found the prevailing opinion is most citizens don’t see any benefit to one and prefer traditional methods.

“This finding also suggests that convincing some users of the value added of a CBDC might pose a challenge for policymakers, and more research will certainly be needed in this area.

“We demonstrate that a substantial portion of consumers report that they would likely not adopt the digital euro, primarily due to a strong preference for an existing payment method. These results suggest that clear communication about the digital euro’s key practical features is essential to encourage broader adoption.”

Per the paper’s abstract, “We also show that when presented with a positive wealth shock of €10,000, consumers tend to allocate only a small portion of this additional liquidity to the digital euro. At the same time, their portfolio allocation across alternative, traditional liquid assets—including cash, current accounts, and savings accounts—remains largely unchanged. In addition, our findings show that holding limits within the range of €1,000 to €10,000 have minimal impact on the composition of consumers’ liquid asset portfolios. Moreover, there is virtually no bunching of the digital euro amount at thresholds of €3,000 or more.”

The ECB believes through better targeted video messaging and education it can help sway opinion, while acknowledging that most of the “financially literate” are only concerned about doing the research.

“We find evidence that consumers who are shown a short video providing concise and clear communication about the key features of the digital euro are substantially more likely to update their beliefs about this new form of payment, which, in turn, increases their immediate likelihood of adopting it compared to an untreated control group. In addition, when consumers are given the cost-free option to learn more about CBDC after the short video, most choose not to do so. Consumers interested in learning more about the digital euro are mainly the more financially literate and higher educated ones for whom information acquisition costs tend to be lower compared to their less literate and less well-educated counterparts.”

On top of this, last month the ECB’s Target 2 (T2) payment system went down for a period of time, preventing banks from transacting for most of the day after the issue was misdiagnosed. Thus, as Reuters noted, those within the EU are questioning whether the ECB could even pull off a digital euro. The outlet reported:

Representatives from four of the eight groups that make up the European Parliament said the incident raised some questions about the ECB’s ability to deliver on its digital euro project, a new payment system open to all euro zone residents.

"This instance is a blow to the ECB’s credibility," said Markus Ferber of the European People's Party, the largest group in the current parliament.

"People will ask legitimate questions how the ECB will be able to run a digital euro when they cannot even keep their day-to-day operations running smoothly."

An ECB official said a digital euro would be more similar to its instant payment system TIPS, which is also 24/7 and handles millions of small payments every day, than to T2, which settles fewer but bigger transactions, and the former has been extremely reliable.

In response to criticism, an ECB spokesperson explained, "The recent outage doesn’t undermine the robustness of the digital euro infrastructure, which is being designed to guarantee that payments continue to function smoothly for users, even when technical issues arise."

In the meantime, the ECB is currently accepting votes on new designs for its banknotes - “European culture” or “Rivers and birds.”

AUTHOR COMMENTARY

As a reminder, don’t forget Lagarde is a convicted thief when she headed the International Monetary Fund (IMF) and was never put in jail: she just got a new job as the head of the ECB.

From The Guardian:

Christine Lagarde has been found guilty of negligence in approving a massive payout of taxpayers’ money to controversial French businessman Bernard Tapie but avoided a jail sentence.

A French court convicted the head of the International Monetary Fund and former government minister, who had faced a €15,000 (£12,600) fine and up to a year in prison. But it decided she should not be punished and that the conviction would not constitute a criminal record. On Monday evening the IMF gave her its full support.

The verdict came as a surprise as even the public prosecutor had admitted the evidence against Lagarde was “weak” during a five-day trial last week. Jean-Claude Marin told the court Lagarde’s actions fell into the category of politics and not criminality and called for her to be acquitted.

Lagarde, who has always argued she did nothing wrong and acted “in the public interest”, was not present for the judgment. Her lawyer Patrick Maisonneuve said she had flown back to Washington DC, where the IMF is based.

‘Crime doesn’t pay,’ they say, or does it? - So keep this in mind when you listen Lagarde spout her rhetoric.

But after announcing she wants the digital euro in October, a week later the ECB is forced to admit that hardly anyone sees a purpose for it (no kidding!). But in all of their hubris and moxie, basically say that the public is not “financially literate,” which I suppose is true, but then essentially admit that they are going to propagandize the masses even more to get them to accept the CBDC, digital ID and tokenization. This means, as far as I am concerned, by hook or by crook they will force it on people;

So we can expect false flag operations to transpire. i.e., ‘Oh, Putin hacked our banking system and all your money is gone, so now we need to create a new financial framework that is more resilient so evil Putin can’t harm us ever again: we’ll show him, we’ll show him how resilient Europe is!” How much you want to bet this is what they might say preceding the enforcement of the digital IDs and CBDCs?

This also fits the timeline for when the Society for Worldwide Interbank Financial Telecommunication (SWIFT) announced they plan to have their systems ready to facilitate CBDCs, in 2025 or 2026:

SWIFT Banking System To Launch CBDC And Tokenized Platform, Expected To Be Released By 2025 Or 2026

The world is racing to adopt CBDCs, stablecoins and tokenization… as if everything surrounding it is just a clever masquerade and world leaders, central banks and private asset managers, are actually working in concert together? After all, the whole world shutdown years ago with mere words and all enacted draconian policies for our “health and safety.” Oh, but this is “conspiracy talk:” silly me for daring to suggest this…

However, the U.S. is appearing to take the stablecoin route instead of CBDCs, which, Lord willing, I will be discussing soon. But if you recall my tokenization essay from last year (which I will be updating with more new information at some point), a stablecoin operates similarly to a CBDC, the difference being it is privatized instead of being held by a central bank. So be careful not to fall for the hoopla that Trump is fighting the deep state.

While it appears we still have a few years to go yet, we are increasingly getting closer towards the eventual mark of the beast.

Revelation 13:16 And he causeth all, both small and great, rich and poor, free and bond, to receive a mark in their right hand, or in their foreheads: [17] And that no man might buy or sell, save he that had the mark, or the name of the beast, or the number of his name. [18] Here is wisdom. Let him that hath understanding count the number of the beast: for it is the number of a man; and his number is Six hundred threescore and six.

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

I still remember the European forum a few years back about which countries would survive the coming global system and which ones would fail. When asked what would happen to the United States of America, Christine Legarde hushed the question and said, “We have other plans for the United States that we can’t talk about here.”

Christine Lagarde may avoid accountability in this life, but ultimately, she'll pay with her own soul. Hell is hot, and she won't escape.