SWIFT Banking System Debuts Tokenization, CBDC And Stablecoin Blockchain Trading Platform

The Trump administration is actively working and preparing their stablecoins, digital dollars, to be tradeable on the updated SWIFT network.

Yesterday, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) formally announced the launch of a new integrated blockchain ledger to facilitate cross-border trade between nations with tokenized assets, including central bank digital currencies (CBDCs) and stablecoins.

SWIFT is the largest international banking network that facilitates transactions and interbank lending between nations. It connects over 11,500 banks and institutions in more than 200 countries and manages trillions of dollars’ worth of transactions per day. In more recent years, it has been used as a cudgel to sanction countries such as Russia, prohibiting a number of Russian entities from transferring and receiving money through the network.

In March last year, SWIFT announced its plans to launch its CBDC trading network sometime in 2025, after it had completed what it claimed was “one of the largest known CBDC experiments to date,” The WinePress reported at the time.

SWIFT claims their “experiments found that our interlinking solution has the potential to simplify and speed up trade flows, unlock growth in tokenized securities markets, and enable efficient FX settlement. And this, all while allowing financial institutions to make use of their existing infrastructure.”

SWIFT says “We plan to extend our solution to support a wider range of emerging digital networks, in addition to CBDCs, such as platforms for tokenized deposits.”

Lewis Sun, Global Head of Domestic and Emerging Payments, Global Payments Solutions at HSBC, said in a statement:

“The ability to interlink emerging and existing market infrastructures is essential to realizing the potential benefits brought on by tokenization and CBDCs. HSBC is excited to continue the collaboration with Swift and other industry peers to incubate an open, inclusive and technology-agnostic model that allows for more efficient payment-versus-payment, delivery-versus-payment, and trade settlement across different networks.”

Today, the international banking system made good on its initial promises and released its blockchain-based ledger. SWIFT has partnered with 30 different commercial banks around the world in “designing and developing a shared digital ledger, with the first use case focused on real-time, 24/7 cross-border payments.”

These banks include:

Absa

Akbank

ANZ

Banco Santander

Bank of America

Banorte

BBVA

BNP Paribas

BNY

Bradesco

Citi

Commerzbank

Crédit Agricole

DBS Bank

Deutsche Bank

Emirates NBD

First Abu Dhabi Bank

FirstRand Bank

HSBC

Itaú Unibanco

JP Morgan Chase

Mizuho

MUFG

NatWest

OCBC

Royal Bank of Canada

Saudi Awwal Bank

Shinhan Bank

Societe Generale-FORGE

Standard Chartered

TD Bank Group

UOB

Wells Fargo

Westpac

Javier Pérez-Tasso, CEO of SWIFT, said in a remark:

“You may think, ‘Wow, aren’t those opposites? Swift and blockchain. TradFi and DeFi. Can they really go together?’ In the regulated system of the future, we believe they can. Banks are ready for it. And they’re asking us to play a bigger role.

“I'm very pleased to announce that we will add a blockchain-based ledger to our technology infrastructure to allow for trusted movement of tokenised value across the digital ecosystems.”

SWIFT debuted the news at the SIBOS international banking and financial conference in Frankfurt, Germany, where Pérez-Tasso provided additional insights. While on stage, he told the audience there is “a huge buzz around the future of tokenized assets and obviously on the back of new policy frameworks, driving momentum around CBDCs and stablecoins.”

He added, “Our focus will be on the infrastructure layer. The types of tokens exchanged on the ledger, the money layer, this is the territory of commercial and central banks.”

Per the press release,

The blockchain-based shared ledger - a secure, real-time log of transactions between financial institutions - will start with a conceptual prototype with Consensys. It will record, sequence and validate transactions and enforce rules through smart contracts. The ledger will be built for interoperability, both with existing and emerging networks, while maintaining the trust, resilience and compliance synonymous with Swift and critical to the secure functioning of global finance.

The ledger will extend Swift’s financial communication role into a digital environment, facilitating banks’ trusted and scalable movement of regulated tokenised value across digital ecosystems. Swift’s focus is on the infrastructure – the types of tokens that will be exchanged on the ledger is the territory of commercial and central banks and Swift will work with them on how to complement and make use of this new infrastructure.

It is envisaged that the ledger -- a secure, real-time log of transactions between financial institutions -- will record, sequence and validate transactions and enforce rules through smart contracts. It will be built for interoperability, both with existing and emerging networks, while maintaining the trust, resilience and compliance synonymous with Swift and critical to the secure functioning of global finance.

In the press release, Anith Daniel Group Head of Transaction Banking Services, Emirates NBD, described this move as “shaping the future of banking.”

Guénolé de Cadoudal, Head of Digital Assets Group at Crédit Agricole in France said:

“Swift’s digital ledger initiative is a promising piece of the digital money network. Through the Swift community, banks and clients will more easily reach convergence on standards for the tokenized representation of money and its integration with the tokenized asset classes. We look forward to contributing with our expertise and business-oriented development.”

Lim Soon Chong, Group Head of Global Transaction Services at DBS Bank added:

“We believe blockchain technology can usher in the next generation of ‘always-on’ and ‘smarter’ financial services. Swift’s initiative goes a step further – it is interoperable with traditional correspondent banking rails, has a high transaction capacity within a secure environment, and is accessible by Swift’s global banking network. These characteristics are critical in supporting broad-based reach and adoption, and have the potential to form the backbone of a resilient and future-ready global financial infrastructure.”

Furthermore, José Luís Calderón, CEO of PagoNxt Payments, highlighted the importance of this operation:

“Traditional international payments models are no longer suited to today’s digital economy. Instead, in sectors like P2P payments and small-to-medium-enterprise (SME) commerce, there is a strong need for faster, more efficient crossborder solutions.

“Tokenization and blockchain technologies enablement of real-time payments, greater transparency, and financial inclusion - all signal ‘the rise of a new global payments paradigm’. This initiative is a great step forward in this direction and we are thrilled to take part in this joint industry effort.”

Stablecoins will also have their place in the SWIFT system. Jean-Marc Stenger, CEO of Societe Generale-FORGE, a French-based investment firm and digital asset provider, touted the benefits of SWIFT’s new system when it comes to stablecoin trading.

“As a stablecoin issuer, we are delighted to join this coalition to further expand the accessibility to regulated tokenized assets, and more specifically Mica-compliant stablecoins, for various use cases. Building on the work already undertaken with our respective teams in previous test transactions, this initiative is fully aligned with our commitment to offer clients robust and widely accessible market infrastructure alongside a new pathway for the digital financial industry.”

Stablecoins are the direction the U.S. is going instead of a CBDC. Stablecoins, as we explained before in detail, effectively act identically to a CBDC but the stablecoins, in this case tokenized, programmable digital dollars, are privatized and managed by third-party entities and financial institutions, which then link back to the Treasury and the Federal Reserve.

Earlier this month, The WP reported on the Trump administration’s aspirations to transition to full tokenization of assets, establish stablecoins as a money replacement, and launch digital IDs, as laid-out in detail in a 166-page report called “Strengthening American Leadership In Digital Financial Technology.” In it, the report mentioned how stablecoins would trade and operate within the SWIFT system.

The authors of the paper wrote (emphasis mine):

A promising use case for stablecoins and other new forms of money is cross-border payments and financial transactions. A wide range of jurisdictions, private sector groups, and international organizations are engaged in initiatives to improve cross-border payments. Some aim to improve the current regime for cross-border payments, to which the U.S. dollar and U.S. financial institutions are central, while other projects may aim to transform global payments to the detriment of the United States.

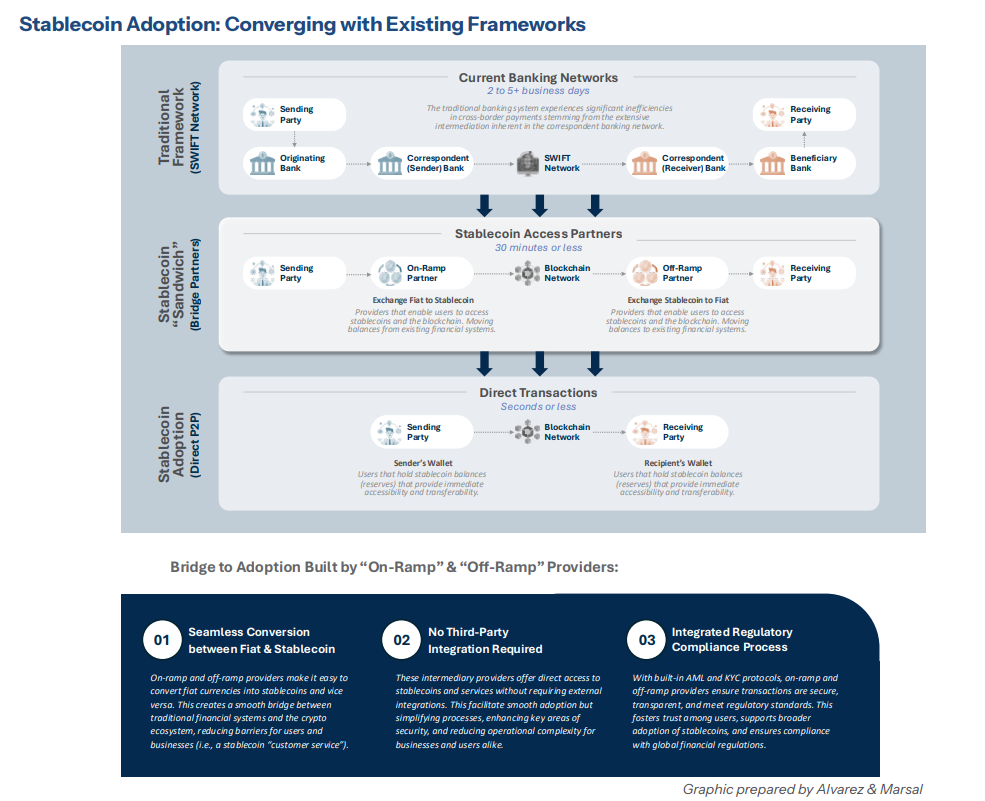

International payments are mainly conducted via the correspondent banking system, in which the primary participants are large banks and financial intermediaries with access to U.S. dollar clearing services and liquidity. Smaller institutions typically access this system through accounts at larger banks. Participants send payment instructions and confirmations through specialized messaging systems, like that operated by the Society for Worldwide Interbank Financial Telecommunication (SWIFT). Payments ultimately settle on commercial and central bank balance sheets, often on a net basis at predetermined times of day for reasons of operational and liquidity efficiency. A single payment may travel across several bank balance sheets and require reconciliation all along the chain in a complex system that has evolved over decades.

In many FX transactions between two non-U.S. currencies, the original currency is converted first to U.S. dollars and then to the final currency, because it is often cheaper than a direct conversion or because there is higher liquidity for conversion to or from the U.S. dollar. This explains the U.S. dollar’s dominant role in FX transactions, and why U.S. institutions and U.S. dollar accounts are central to cross-border payments. This centrality incentivizes foreign financial institutions to implement U.S. sanctions and maintain robust AML/CFT controls, both of which are key U.S. economic and national security tools.

Digital asset proponents are applying the full suite of new money-like products to cross-border retail payments. Digital assets and stablecoins already flow across borders, although the evidence indicates that, except for in select countries, these flows predominantly finance activity within the global digital asset ecosystem.

Large-value wholesale cross-border payments can also benefit from the advantages of digital assets and DLT. While some of this work advances piecemeal upgrades or technical improvements to existing systems, there is significant interest in designing new multilateral [Financial Market Infrastructures] FMIs or common platforms for cross-border payments. In its most ambitious form, a new FMI would accommodate varied types of tokenized assets traded across borders.

AUTHOR COMMENTARY

It’s amazing to see these developments taking place quite rapidly and very subtly, yet there is hardly an ounce of coverage and discussion about this. It’s right in front of our faces. The whole world is moving in this direction, the entire world…

Don’t lose sight of that as Western and international media pin each other against one another, as world governments in collaboration with multilateral interest groups and central banks collude to tokenize everything; turning everything, including you and I, into a programmable, trackable, traceable, speculative asset on a blockchain 24/7/365 with built-in permissions, conditions and detailed records.

Proverbs 22:7 The rich ruleth over the poor, and the borrower is servant to the lender.

And once again, we are reminded that the Trump administration is working overtime behind the scenes and yet in broad daylight to usher in this system; giving us serfs the privilege of holding and ‘owning’ what they openly define as “money-like objects.” Notice that - notice how they cannot call it money, because it is not: it’s a programmable token that pretends to be money.

But as the dollar dies by design, this hyper-inflationary event will be used to drive on-boarding to get the terrified masses “on-chain.”

Notice how these stablecoins are also apparently able to trade and work with other countries’ CBDCs. If that is not proof enough that a stablecoin is no different than a CBDC in function…

It’s another brick in the road marching the world closer to the end stage final solution.

Revelation 13:16 And he causeth all, both small and great, rich and poor, free and bond, to receive a mark in their right hand, or in their foreheads: [17] And that no man might buy or sell, save he that had the mark, or the name of the beast, or the number of his name. [18] Here is wisdom. Let him that hath understanding count the number of the beast: for it is the number of a man; and his number is Six hundred threescore and six.

The Lord Of Glory: The Detailed Guide To Who God Is – Available Now!

On one of his missionary journeys, the apostle Paul visited Athens, Greece, where he said he witnessed “the city wholly given to idolatry,” and who were “too superstitious” and worshipped a plurality of gods and deities, though the people acknowledged that there was still one God above all that was a mystery to them. When questioned by the philosophers …

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Reason number 346 why I moved to CHILE, a free....first-world nation in South America eleven years ago. Gun ownership is legal and chemtrailing never ever has been done here. ALL

beef is free-range (grass-fed; no corn)

and minus growth hormones/antibiotics.

Same goes for chickens. Zero factories.

They eat alfalfa, clover, worms, insects, seeds, etc. WORLD'S HUGE SECRET.

DJT said NO CBDC. He's clearly the Trojan horse controlled by palantir & big $$$$$$$$. Traitor to MAGA.