🚨Financial Freedom Is Over: CBDCs Now Legal In US. Trump Signs Bill That Establishes Stablecoins As Digital, Programmable Money

Stablecoins are privatized CBDCs by another name and are arguably worse because of it. This paves the way for full-blown tokenization of everything. The digital chains are here ⛓️

While the nation has been distracted and overwhelmed with the shock and awe surrounding the Jeffrey Epstein fiasco, major legislation was just passed that changes the financial landscape forever. The United States has passed several pieces of legislation during what has been dubbed “Crypto Week,” which establishes the public and private integration of digital, programmable ‘money’ as stablecoins, integrated on a blockchain. While the legislation claims to protect against the creation of a central bank digital currency (CBDC), these bills essentially still create a CBDC but call it by another name.

Though most Americans have yet to realize it, the financial ecosphere has changed forever as the country and the world enters a new age of what is considered money, and how regular citizens will interact with it and be forced to live with these new rules.

The WinePress has noted several times this year that the Trump administration is moving quickly to deregulate the banking and crypto sectors, and working towards implementing the rapid digitization of money and financial systems.

In March, Trump signed two executive orders that overhaul the Treasury Department by eliminating cash and check payments. I noted at the time that these executive orders referenced utilizing instant-transfer payment rails such as FedNow, which lays the foundation for tokenized money and assets. The Biden White House and the Federal Reserve have previously admitted that FedNow would be used to facilitate the transaction of a CBDC. Trump’s executive orders claimed that they were not creating a CBDC, but the actions taken indicated the opposite.

Moreover, Trump’s One, Big, Beautiful Bill creates “Trump Accounts,” essentially baby bonds by another name. These accounts are created and managed by the Treasury - the same Treasury that was overhauled months prior to be digital - and those direct deposits then come directly from the Federal Reserve into those accounts; effectively creating a CBDC.

There are three bills that were passed this week, each interconnected with each other. We will breakdown each one and what it means and what some of its effects are.

It is worth noting that President Donald and Treasurer Scott Bessent have both openly expressed their support for these bills. Bessent said in May, “We believe the United States will be the premier destination for digital assets. Digital assets are an important source of innovation that can drive usage of the U.S. dollar around the world with stablecoin legislation.”

Last month, Vice-President JD Vance declared that “There’s a new sheriff in town,” vowing that the administration would fire anyone who was not on board the crypto train.

“In this administration, we do not think that stablecoins threaten the integrity of the United States dollar, quite the opposite. In fact, we view them as a force multiplier of our economic might. […] It’s a hedge against skyrocketing inflation, which has eroded the real savings rate of Americans over the last four years.”

The GENIUS Act

“S.1582 - GENIUS Act” creates a framework for stablecoins. It has been debated in the Senate for months before it was adopted on Wednesday. The U.S. Senate Banking Committee passed it in March, and after some delays and amendment discussions, the Senate formally passed the bill in June. The House stayed-up late on Wednesday in an historic ten-hour voting session, resulting in a 308 - 122 vote.

A summary of the bill states:

This bill establishes a regulatory framework for payment stablecoins (digital assets which an issuer must redeem for a fixed value).

Under the bill, only permitted issuers may issue a payment stablecoin for use by U.S. persons, subject to certain exceptions and safe harbors. Permitted issuers must be a subsidiary of an insured depository institution, a federal-qualified nonbank payment stablecoin issuer, or a state-qualified payment stablecoin issuer. Permitted issuers must be regulated by the appropriate federal or state regulator. Permitted issuers may choose federal or state regulation; however, state regulation is limited to those with a stablecoin issuance of $10 billion or less.

Permitted issuers must maintain reserves backing the stablecoin on a one-to-one basis using U.S. currency or other similarly liquid assets, as specified. Permitted issuers must also publicly disclose their redemption policy and publish monthly the details of their reserves.

The bill specifies requirements for (1) reusing reserves; (2) providing safekeeping services for stablecoins; and (3) supervisory, examination, and enforcement authority over federal-qualified issuers.

The bill allows foreign issuers of stablecoins to offer, sell, or make available in the United States stablecoins using digital asset service providers, subject to requirements, including a determination by the Department of Treasury that they are subject to comparable foreign regulations.

Under the bill, permitted payment stablecoins are not considered securities under securities law. However, permitted issuers are subject to the Bank Secrecy Act for anti-money laundering and related purposes.

Read the White House fact sheet here.

Trump signed the bill earlier today.

During Trump’s signing of the Genius Act into law, a number of crypto executives were center stage at the event, including Kraken co-CEO David Ripley, Gemini co-founders Cameron and Tyler Winklevoss, Coinbase CEO Brian Armstrong, Circle CEO Jeremy Allaire, Tether CEO Paolo Ardoino and Robinhood CEO Vladimir Tenev.

“The entire crypto community, for years, you were mocked and dismissed and counted out, you were counted out as little as a year and a half ago, but this signing is a massive validation [...] of your hard work and your pioneering spirit,” Trump said in a speech.

He added:

"I pledged that we would bring back American liberty and leadership and make the United States the crypto capital of the world. And that's what we've done. And under the Trump administration, this is only going further.

"Just as I promised last year, the GENIUS Act creates a clear and simple regulatory framework to establish and unleash the immense promise of dollar-backed stablecoin. This could be perhaps the greatest revolution in financial technology since the birth of the internet itself."

Commissioner Hester Peirce, who also leads the Securities and Exchange Commission’s (SEC) crypto task force, said in an added statement: ”People have voted with their dollars—privately issued stablecoins already enjoy broad use as a payments mechanism. The GENIUS Act, by putting a regulatory framework around them, aims to protect current and future users and the financial system.”

Cointelegraph noted: The law will come into effect 18 months after Trump signs it, or 120 days after the so-called “primary federal payment stablecoin regulators,” including the Treasury and Federal Reserve, issue final regulations implementing the GENIUS Act.

More on this bill later…

Clarity Act

“H.R.3633 - Digital Asset Market Clarity Act of 2025” provides legislation that establishes a market structure for cryptocurrencies and digital assets traded on a blockchain. The bill passed in a 294-134 congressional vote. It now goes to the Senate for a vote. The text reads:

This bill establishes a regulatory framework for digital commodities, defined by the bill as digital assets that rely upon a blockchain for their value.

The Commodity Futures Trading Commission must generally regulate digital commodities transactions, including digital commodity exchanges, brokers, and dealers. To qualify for trade on an exchange (1) a digital commodity’s blockchain must be mature, or on a blockchain system that has achieved decentralized control as defined by the bill; or (2) the issuer of the digital commodity must file certain reports. The bill establishes requirements for trade monitoring, recordkeeping, and the commingling of customer assets.

The bill exempts digital commodities on mature blockchains (and digital commodities on blockchains expected to mature within certain timeframes) from Securities and Exchange Commission (SEC) registration requirements if annual sales fall under a certain amount and other requirements are met. The bill provides the SEC with jurisdiction over digital commodity activities and transactions engaged in by certain brokers and dealers on alternative trading systems and by national securities exchanges.

Digital commodity exchanges, brokers, and dealers are subject to the Bank Secrecy Act for anti-money laundering and related purposes.

The bill also sets forth requirements for alternative trading systems, previously issued digital commodities, and provisional registration until the bill is implemented.

“The Clarity Act helps us get there by adding consumer protection into law and setting clear guidelines for digital asset managers,” stated Congressman John Rose. “It also establishes guardrails for federal agencies, who have too often stepped outside their statutory authority in recent years, especially with cryptocurrency. The bill offers modern solutions to a modern financial sector that grows in popularity and relevance by the hour.”

“At present, there is no established market structure to protect consumers or provide clear rules of the road for businesses and innovators,” stated Congressman Don Davis. “It’s the wild, wild west! Congress must deliver market structure legislation that brings clarity. Millions of Americans are holding cryptocurrency, using it in financial transactions, or using other digital tokens as part of new, innovative technologies and services. There must be consumer protections, and the United States must lead.”

Anti-CBDC Act

“H.R.1919 - Anti-CBDC Surveillance State Act” passed in a narrow vote of 219-210 in the House and now goes to the Senate for a vote as well. As implied in the title, the bill claims to ban a CBDC in the U.S.

The text reads:

This bill prohibits a Federal Reserve bank from offering products or services directly to an individual, maintaining an account on behalf of an individual, or issuing a central bank digital currency (i.e., a digital dollar). Further, the Board of Governors of the Federal Reserve System is prohibited from using a central bank digital currency to implement monetary policy or from testing, studying, creating, or implementing a central bank digital currency, with exceptions as provided by the bill.

A CBDC Disguised As Something Else

Even though President Trump and Congress have tried to say that these bills prevent a CBDC, not everyone agrees.

Rep. Marjorie Taylor Green (GA-R) is one of some who is concerned about this legislation and voted against the Genius Act.

She warned in an interview with Steve Bannon’s War Room that these bills do indeed create a CBDC. Bannon tried to defend the bills but MTG was quick to rebut his claims. “The number one thing that is not happening today is a ban on a [CBDC]. This means the ability of the government to take control of your digital bank account, where all your money is, and turn it off. This is why I am so upset and it is not being talked about.” She says that last-minute guarantees given by Speaker Mike Johnson in order to get the bill passed and prevent a CBDC will in all likelihood get stripped from the Senate vote. She pointed out that these bills are designed to switch Americans over from cash to programmable tokens that can be tracked and traced by the central government. She referenced Revelation 13:16-18 and the prophesied future of the mark of the beast, and in good conscience said she could not support these bills.

Buried in the text of the Genius Act, the legislation clarifies how these private regulators can manage the stablecoins. One of the provisions granted explicitly allows these third-party custodians to place restrictions and freezes on the money at their discretion. It reads (emphasis mine):

A permitted payment stablecoin issuer shall be treated as a financial institution for purposes of the Bank Secrecy Act, and as such, shall be subject to all Federal laws applicable to a financial institution located in the United States relating to economic sanctions, prevention of money laundering, customer identification, and due diligence, including-

(i) maintenance of an effective anti-money laundering program, which shall include appropriate risk assessments and designation of an officer to supervise the program;

(ii) retention of appropriate records;

(iii) monitoring and reporting of any suspicious transaction relevant to a possible violation of law or regulation;

(iv) technical capabilities, policies, and procedures to block, freeze, and reject specific or impermissible transactions that violate Federal or State laws, rules, or regulations;

(v) maintenance of an effective customer identification program, including identification and verification of account holders with the permitted payment stablecoin issuer, high-value transactions, and appropriate enhanced due diligence; and

(vi) maintenance of an effective economic sanctions compliance program, including verification of sanctions lists, consistent with Federal law.

This echoes language used in Trump’s March executive orders to revolutionize the Treasury, which states:

The Secretary of the Treasury shall support agencies’ transition to digital payment methods, including by providing access through the Department of the Treasury’s centralized payment systems to:

(i) direct deposits;

(ii) debit and credit card payments;

(iii) digital wallets and real-time payment systems; and

(iv) other modern electronic payment options.

These similar stop-gap and policing measures are the same capabilities granted to banks with the Federal Reserve’s instant-transfer payment system FedNow; which was referenced in Trump’s executive order earlier this year as a tool to retrofit the Treasury Department by going cashless. Cleveland Federal Reserve President Loretta Mester explained the power banks would have with FedNow:

“It is true that FedNow and other payment services can be used to move money; however, banks have tools they could use to mitigate large outflows of deposits. For example, within FedNow they could lower their transaction limit, restrict access to the service to certain non-wholesale customers, or change to “receive payments only” status. They could also design their own controls to limit the total volume of transfers to manage their risks while serving their customers.

“Future releases of the FedNow Service may allow configurable transaction limits by customer type, if such limits are deemed useful. In addition to a bank being able to borrow from the Fed during the hours the discount window is open, a bank could use liquidity management transfers to replenish its master account balance from private funding sources on the weekend when the discount window is not accessible, which would help to mitigate the effects of deposit outflows on the health of the bank.”

Logan Payne, a crypto-focused lawyer at Winston & Strawn, told Cointelegraph that the GENIUS Act creates an incentive for stablecoin issuers to seek a banking license.

He said a new stablecoin license under the GENIUS Act limits a company’s activities to “purely stablecoin issuance,” but most stablecoin issuers do more than that. “Pretty much every stablecoin issuer in the United States issuing under US law right now engages in activities outside the scope of that license,” Payne said.

Even if an issuer gets a GENIUS Act-approved license, Payne said they’d still need state-level money transmission licenses to operate nationally.

That creates an incentive for stablecoin issuers to apply for a national trust bank charter with the Office of the Comptroller of the Currency (OCC), like Circle and Ripple have done, “which allows for them to engage in stablecoin issuance plus a wider range of activities, but without having to get state-to-state licenses,” he said.

Circle manages the USDC stablecoin - a tokenized representation of the U.S. dollar.

Though this administration has repeatedly lambasted CBDCs and has tried to assuage the public that they are not creating a CBDC, a stablecoin, for all intents and purposes, is a CBDC by another name; the only real difference being that one is operated by a central bank, the other being managed by third-party entities and corporations who can then act as their own bank and custodian of these currencies.

In March, Bitcoin Magazine explained how stablecoins are hardly different from a CBDC. While the author is biased in favor of Bitcoin, he still explains how a stablecoin is still a CBDC.

The author wrote:

All of the stablecoin volume of significance happens on highly centralized blockchains, issued through highly centralized smart contracts that almost entirely (with rare exceptions like Liquid currently) have the power to arbitrarily freeze or confiscate any outstanding stablecoin tokens. A single party, the issuer, for the super majority of tokens they have issued, can freeze and seize their funds. Anywhere. Anyone. Globally.

These blockchains almost all function on an account model as well, meaning that default behavior associates every transaction a user makes with a single public address identifier, putting their entire transactional history in full view of the world with a single glance. No UTXO clustering, no fancy analysis needed, just look at the account address.

To compound things even further, because all of these chains are highly centralized, there is no software to speak of that general users interact with that is fully validating. Wallets connect to one of a few highly centralized servers every time they interact with their account and associate their IP address with that account.

This is a trap. Pure and simple. The United States does not need a CBDC, it has US Dollar stablecoins. They already function in a way that concentrates all private information that could connect individuals to their on-chain activity in a few hands. All it takes is one interaction with a KYC exchange, or an address posted online, connection to a social media account, and you’re identified.

Stablecoins are just as programmable as a CBDC. Just as capable of implementing restrictions like expiring money, or money that can only be spent in certain ways or certain places. What’s the only difference between the two that matters? Adoption. Stablecoins are viewed favorably, and highly used, whereas most places the sentiment is very against CBDCs.

All of the pieces are there. The central point of control to seize the tokens, the total lack of privacy that makes a single association of KYC data a permanent surveillance mark, and the complete concentration of where that private information will wind up. All there to be snatched up and collected by the US government whenever it wants, and used to coerce stablecoin issuers into acting how they see fit.

These stablecoins are US dollar proxies, they must interact with the legacy financial system, they have to hold actual dollars and treasuries. It is necessitated by how they work. They are under the government’s thumb, particularly the US government’s thumb, whenever the government wishes it.

CBDCs are a bogeyman to keep us distracted from the very real threat of a financial surveillance system that’s already here, stablecoins. We should be confronting that, not sweeping it under the rug.

Bitcoin Magazine editor Mark Goodwin said something similar in April:

“Stablecoins are the bait and switch for direct-issued government CBDCs.”

“Stablecoins can be programmed. Exactly like how we fear CBDCs will be programmed. They’re exactly the same tokenized mechanism… They can be taken out of your wallet. Your wallet can be blacklisted. A lot of the things that we fear about CBDCs are totally available within the tool set of Stablecoins.”

Moreover, Trends Journal contributor and stock market analyst Gregory Mannarino has sounded-off about this recent move by the government.

He described this as “Trump’s executive order banning a CBDC was sleight of hand, a magician’s misdirection. While the crowd cheered "He’s protecting our freedom!", he quietly opened a side door…” He added (emphasis his):

What are these [stablecoins]? Privately issued digital dollars backed by fiat, controlled by private companies. Regulated by the Federal Reserve and Treasury. And Now we get DIGITAL SLAVERY THRU ANOTHER DOOR… No privacy. No accountability. No limits on tracking or control.

AMERICA FIRST FOR WHO?

For the Fed, who still controls the system. For the 1%, who profit from the tech, regulation, and surveillance architecture. For the People? Bread and Digital Circuses.

THE DECEPTION DECODED…

“No CBDC?” Trump’s “ban” simply shifted the label, not the outcome. He rebranded the digital dollar with stablecoins.

The Stablecoin Con. “Stable” to WHAT? They're pegged to the US dollar, which itself is backed by… nothing but debt. So it’s a token pegged to another dying token. ITS A CON NESTED INSIDE A CON!

Moreover, Mannarino argues that stablecoins are even worse than an ordinary CBDC. “This is in reality A WORST CASE SCENARIO… We would have been better off with a direct CBDC,” he warns. He provides 6 reasons why:

1. Illusion of Choice… Total Control.

These corporate stablecoins masquerade as “free market innovation,” giving people the illusion that they are using a decentralized or private alternative to government money. But behind the curtain? The Fed and Treasury still pull the strings.

2. No Congressional Accountability.

A Fed CBDC would require direct Congressional approval and would spark massive public debate. But corporate issued stablecoins can be rolled out without public oversight!

3. Built-in Surveillance by Proxy.

When private firms issue “money” as these stablecoins, but the Fed regulates the flow, the government gains full surveillance capability without ever appearing on your bank app. The Fed watches from behind the veil, with no fingerprints.

4. Programmability and Blacklisting.

These stablecoins can be programmed just like a CBDC… Transactions denied based on social score, location, spending habits. Wallets frozen “for security concerns.” Cross platform tracking (shopping, browsing, travel). All without ever passing a law.

5. Corporate Profiteering + State Tyranny = Babylon Hybrid Beast.

This is THE unholy alliance. Corporate tech giants and the central banking system merging into one. The corporations profit from adoption. The Fed enforces compliance. The people? Locked in digital servitude.

6. Trump’s Trojan Horse

Trump publicly rejects CBDCs… but supports corporate stablecoins regulated by the Fed? Sure, this appeals to conservatives and crypto fans alike but it’s the same beast.

Catherine Austin-Fitts, former Assistant Secretary of the US Department of Housing and Urban Development (HUD) under President George Bush Sr., has long warned about the digital control grid and tokenization of assets being ushered in, and what it would mean for freedom for people around the world.

In May, she warned:

“He (Trump) is moving very, very fast…

“[…] He said no CBDC’s… I don’t know if you’ve read the Genius Act which is the new plan for stablecoins - a CBDC if issued would be issued by the Federal Reserve…..

…The guys who own the New York Fed are all going to create subsidiaries and issue stable coin which will be interoperable and can work with a social credit system…”

In April, Austin-Fitts warned that what was coming was not technocracy but “slavery,” believing that Trump was reinserted because the central bankers believed the last administration was not getting the job done adequately.

"And I would say that the current administration was put into place by the bankers to get the control grid accomplished. The last group couldn't accomplish the control grid. This group is doing a remarkable job of implementing the control grid at high speed, and marketing it. And I would say both the Democratic and Republican side do not see the digital concentration camps snapping into place around them, and it's shocking.

"It's not technocracy. It's slavery. I mean, it's, you know, I think it'll have a different face and feeling in Europe than in the United States, but in the United States, we're talking about slavery. And we're talking about, you know, I have said that if you look at the, you know, one of the reasons we can get rid of USAID is we don't need soft power anymore because with drones and robots and invisible weaponry and surveillance systems, you know, we can use hard power very cheaply and economically.

"And if you look at some of the things that have been happening in the United States with using hard power to basically kill people and take their lands, you know, this is very dangerous."

also points out that the ramifications of this bill are wide-reaching and will exact more control over the people. She references how, for example, this could be used to enforce vaccine mandates. She wrote:

“In September 2021, the employees of all federally-funded Medicaid and Medicare-certified health care facilities, and Head Start program facilities, were required to be vaccinated, as ordered through the United States Department of Health and Human Services (HHS).”

Freezing all money earned or inherited by a person, in practical terms, amounts to the confiscation of all assets without due process. Thus not only would have COVID vaccine mandate “refusers” have been devoid of income, upon termination. They also would have been denied access to their savings.

The mandates were not passed by Congress, but by a whim of the Executive Branch under the Biden administration, which also mandated that companies with over 100 employees must show that all their employees were COVID vaccinated in order to be in compliance with federal OSHA regulations.

Similarly, the Executive Branch, whether under Trump or anyone else, has enormous latitude to govern by executive or federal agency regulation, […] Executive Branch dictates can make rules for what constitutes acceptable, “positive” identification, such as requiring facial recognition scans for Real ID, or rules declaring certain public spaces off-limits for protests, such as the Capitol grounds on J6.

AUTHOR COMMENTARY

And NOW you know why the Epstein debacle is being pushed so hard in the media… They needed a massive coverup while they enacted this legislation.

Ladies and gentlemen - today is July 18th, 2025, a day that will go down in quiet infamy, because financial freedom is now dead. The masses have zero idea what is going on and what the ramifications of this will be.

Everything that we have been warning about for years now, the warnings about CBDCs and the tokenization of all assets, have now come to pass… CBDCs are now official.

And now we have something, according to some, that is even worse (if you can imagine it) than just an ordinary CBDC: you now have corporations and private entities that can fake currencies and programmable “money” - money that has regulations, contracts, terms and conditions, expiration dates; track and traceability, real-time surveillance - that can be managed with little oversight; and not just that, but working in tandem with the federal government and the Federal Reserve.

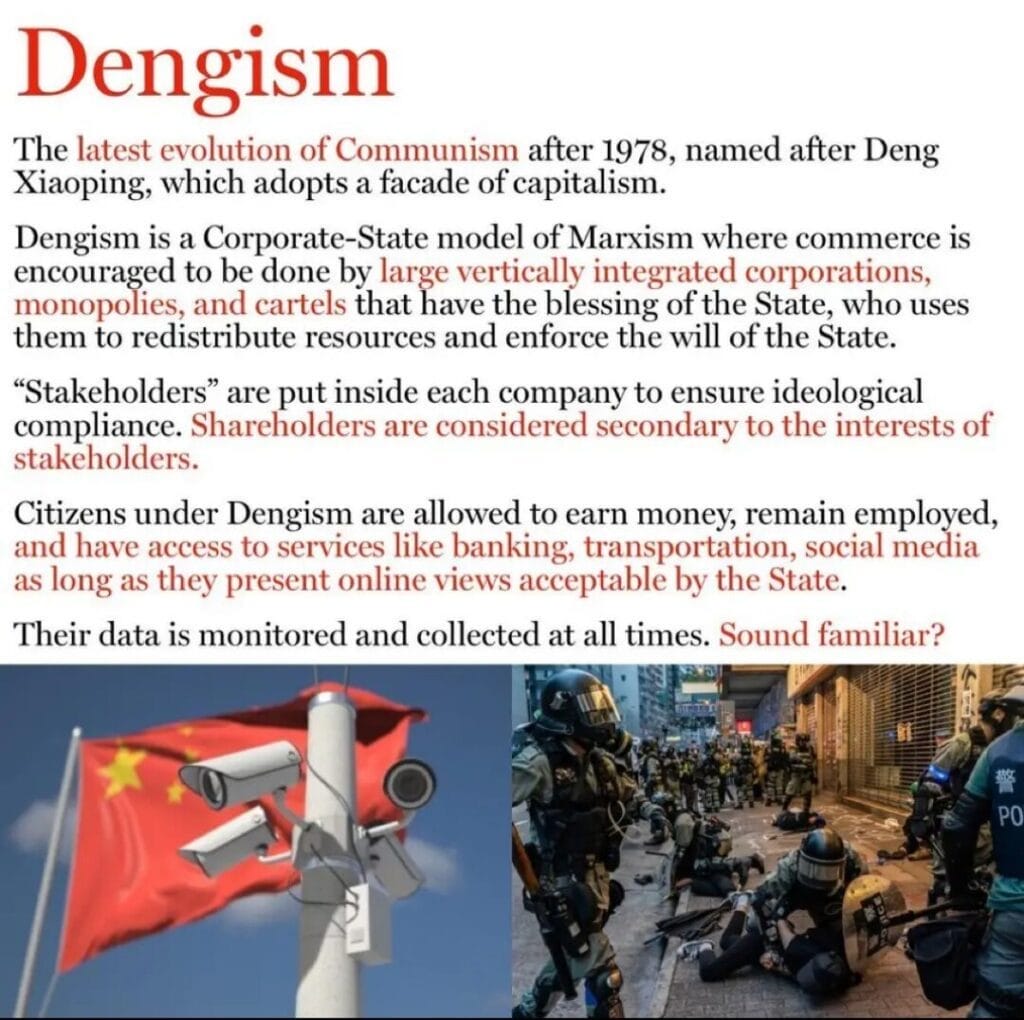

In my very important tokenization essay I published last year (which I will be updating and republishing with even more information very soon, so please stay tuned), I warned of what was coming: Dengism.

Well, it’s here now.

And it’s not just these crypto companies doing this, we have the big boys and other nonconventional companies doing this. Mastercard is building a stablecoin network. JP Morgan is leaning into stablecoins. Then you have BlackRock doing it, which of course Larry Fink is absolutely an advocate for tokenization and Bitcoin as a trojan horse, as I exposed before. But let’s make things even crazier. Even Walmart and Amazon are working on stablecoins! Imagine that, imagine Walmart and Amazon - two of the largest commerce, grocery and supermarket companies in the world - operating as their own “bank”, working in tandem with the Treasury and Federal Reserve, to issue their own fake digital, programmable money that is then tradeable on a blockchain ledger! Fathom that!

We are not returning to a gold-backed system. I know there are all kinds of people online who want to keep selling you that false hope, and that if you buy their products we can stop the rollout and give us leverage, but none of this has or will stop the rollout of stablecoins, CBDCs and tokenization of all assets. As a matter of fact, gold itself is being tokenized by different groups.

Treasury Secretary Scott Bessent, after much hoopla and speculation, said that the Treasury and the Federal Reserve are not going to be revaluing the price of gold to a more fair and realistic value. This came after he said in February, "We're going to monetize the asset side of the U.S. balance sheet." This was then taken to mean by precious metal investors that this meant the Treasury would revalue precious metals to a more proper value. But Bessent shot that down last month as bullion dealers and stackers continue to foment that a revaluation is coming. "I said we're gonna mobilize the asset side of the balance sheet, and all the gold bugs said 'He's gonna revalue the gold!' "I can say today we're not revaluing the gold, but...every department head is looking for the assets that we can mobilize," Bessent said, referencing energy leases and federally-owned land as investments that could be part of a U.S. sovereign wealth fund, versus using a revaluation of the alleged 8,133 tons of gold reserves to release funds for current government spending or paying down the national debt.

Of course, revaluing gold would assume the country even has any to revalue to begin with, and since there is no rush to audit Fort Knox (after both Trump administrations have dangled that carrot already), I am going to assume like most that there is nothing there. That, and gold prices are determined internationally as well, so the U.S. cannot magically reallocate a new price; and even if it did, it would not pay down the debt. Why would the central bank and treasury want to give monetary power back to the people? It’s antithetical to their goals of control. Yet there are still tons of precious metals channels who continue to peddle this ruse. If Trump wanted to return to a gold standard he could very easily with a signature swipe, but he hasn’t and isn’t going to.

So what are these sinister stablecoins backed by then? That’s right, the dollar; a decaying fiat that is backed by nothing. How long can these stablecoins even be sustainable? Or does that not even matter at this point and these people are only interested in creating infinite fairytale money on a screen, while the power elites hodl all the real assets and best land and resources for themselves?

Proverbs 28:3 A poor man that oppresseth the poor is like a sweeping rain which leaveth no food.

Now, interestingly enough, the Bank for International Settlements (BIS), the central bank of central banks, has pushed back against stablecoins. In June, they strongly emphasized tokenization is the future financial monetary system (which is what I have been beating the drum about and warning is coming rapidly - more on this in the future), but said stablecoins are “unsound money.”

“While stablecoins' future role remains uncertain, their poor performance on the three tests suggests they may at best serve a subsidiary role.

“Society has a choice. The monetary system can transform into a next-generation system built on tried and tested foundations of trust and technologically superior, programmable infrastructures. Or society can re-learn the historical lessons about the limitations of unsound money, with real societal costs, by taking a detour involving private digital currencies that fail the triple test of singleness, elasticity and integrity. Bold action by central banks and other public authorities can push the financial system along the right path, in partnership with the financial sector.”

BIS also published another paper this week cautioning on stablecoins and their inherent risks, though Ledger Insights, a publication dedicated to tokenization, says both recent papers by the BIS are biased and do not give stablecoins a fair shake, only highlighting their risks.

This then begs the questions, are stablecoins the endgame, or are they another stopgap measure that bridges us eventually into something even worse…? Or will the United States and a few other countries be mostly isolated from the rest of the world will still digitally enslaving its people in another way?

Of course, there is no question that this has taken us one big leap even closer to the final solution:

Revelation 13:16 And he causeth all, both small and great, rich and poor, free and bond, to receive a mark in their right hand, or in their foreheads: Revelation 13:17 And that no man might buy or sell, save he that had the mark, or the name of the beast, or the number of his name. Revelation 13:18 Here is wisdom. Let him that hath understanding count the number of the beast: for it is the number of a man; and his number is Six hundred threescore and six.

The bottom line, as we have covered, a stablecoin for all intents and purposes IS a CBDC; and that CBDC is here and now; and with that comes the end of freedom and in comes an authoritarian state. Even mainstream media admits it.

Newsweek wrote in 2022:

If the Federal Reserve adopts a central bank digital dollar, the American government will be on a surefire path to authoritarianism.

With an American CBDC, the government would become both money printer and bank, destroying any checks and balances to the governments' power over Americans' financial holdings. By granting the government ownership over the root technology of money, CBDCs allow the government complete discretion over how and whether people can use their money.

By adopting CBDCs, American and Chinese monetary systems would converge—both destroying the financial sovereignty of individuals and luring citizens into a financial mousetrap predicated on a false sense of security, by appropriating Bitcoin's virtues of decentralization and immutability at the expense of unsophisticated account holders.

It is imperative that Americans become aware of the dangerous implications of CBDCs and quell any efforts to develop an American CBDC currently at play in the government, as the Fed prepares to launch its discovery report on CBDCs exploring future applications.

Indeed; so what does the Trump administration do? ‘Don’t call them CBDCs, the public won’t accept them; call them stablecoins (not money) and cry decentralization; down with the Fed, and into a new dawn of financial freedom for all!’ Make American Great Again! Wining, winning, we’re going to win so much you’ll get tired of winning!’

Before Trump and Musk’s pretend feud, what was one of the first things he introduced while at DOGE? Blockchain to bolster the department. In other words, officially build the necessary infrastructure needed to facilitate stablecoins and tokenization. After all, they needed to eliminate that “fraud and waste,” right?

And keep in mind how this whole system aligns with what Musk wants to do, to make X the all-in-one app akin to China’s WeChat, transferring away power from banks to companies such as his. Don’t fall for his fake bickering with Trump: this legislation is a dream come true for Musk. Fact!

David Knight pointed this out in an episode of his show last year when cited my article about tokenization and why it is so dangerous. Watch it here.

As I alluded to in my detailed essay on tokenization last year, people such as Trump, Musk, Javier Millei, and a number of so-called “patriotic” politicians in Europe are being propped up right now to mislead the masses. The American empire, the European Union, the Western hegemon, are collapsing and there is nothing that can be done to stop it. So, as the rich fat cats jump ship and get out before the Titanic sinks, the wealth and power needs to be restructured. But no one wants to hear that their empire is dead and people’s way of living is about to get very difficult more than it already is; so, people like Trump and these other guys are being sent down from “human resources” (metaphorically speaking) to deliver the “bad news,” but they have such a great way of spinning it that they make you think it’s a great opportunity and there is a silver lining. That’s why these leaders are selling this collapse and consolidation with a libertarian, reductionist, patriotic and populist spin.

And with this system, they must continue to collect and harvest our data, all of it.

There is a lot more I could say but I will save that for more reports to follow.

As per the Genius Act, these regulations are officially implemented 120 days from today, which is January 14, 2026. This gives us a window before splashdown when everything truly changes from that day forward.

Indeed, today is a dark day for America, yet hardly anyone will notice…

Last year, I wrote a detailed piece about how “money faileth” and what the scriptures say in this regard, and what we should do. I recommend that you read it or reread it again.

What should come after is beyond me; but this I do know:

Ecclesiastes 7:14 In the day of prosperity be joyful, but in the day of adversity consider: God also hath set the one over against the other, to the end that man should find nothing after him.

2 Timothy 1:12 For the which cause I also suffer these things: nevertheless I am not ashamed: for I know whom I have believed, and am persuaded that he is able to keep that which I have committed unto him against that day. [13] Hold fast the form of sound words, which thou hast heard of me, in faith and love which is in Christ Jesus. [14] That good thing which was committed unto thee keep by the Holy Ghost which dwelleth in us.

Romans 8:31 What shall we then say to these things? If God be for us, who can be against us? [32] He that spared not his own Son, but delivered him up for us all, how shall he not with him also freely give us all things? [33] Who shall lay any thing to the charge of God’s elect? It is God that justifieth. [34] Who is he that condemneth? It is Christ that died, yea rather, that is risen again, who is even at the right hand of God, who also maketh intercession for us. [35] Who shall separate us from the love of Christ? shall tribulation, or distress, or persecution, or famine, or nakedness, or peril, or sword? [36] As it is written, For thy sake we are killed all the day long; we are accounted as sheep for the slaughter. [37] Nay, in all these things we are more than conquerors through him that loved us. [38] For I am persuaded, that neither death, nor life, nor angels, nor principalities, nor powers, nor things present, nor things to come, [39] Nor height, nor depth, nor any other creature, shall be able to separate us from the love of God, which is in Christ Jesus our Lord.

Share this, help get the word out to those who are still willing to listen.

Summer Sale: "The Lord Of Glory: The Detailed Guide To Who God Is" At Discounted Price For Limited Time!

Starting today and ending on July 31st, my book "The Lord Of Glory: The Detailed Guide To Who God Is" is on sale for 15% off its normal listing (prices will vary internationally).

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

Great Reset. We the People were set up yet once again. Seems Trump was given the Midis touch. He was manufactured to bring in the Great Reset. Trump has gone global. Look no further than his global businesses.

Whilst he says he is America first. He’s busy taking his business global. How come no one talks about this?

Every human born in the US is collateral already- birth cert & SS#'s is what all that is about. Americans are really really in the dark, this has already been happening for a long time.