World Bank Publishes Framework On Global Digital ID Verification And Instant Payment Systems Leading To Broader Tokenization

"Fast payment systems have transformed how money moves. The next phase is about how safely, confidently, and inclusively people can use them."

The World Bank recently published proposals for interoperable digital identity verification systems intertwined with instant transfer payment systems and banking.

World Bank officials have previously commented on the need for digital IDs in finance. In 2024, World Bank Group President, Ajay Banga, and Hans Vestberg, Chairman and CEO of Verizon, spoke at the Global Digital Summit in Washington D.C., expressing the need for a digital ID verification system.

Banga referred to digital IDs as “the social contract of a citizen” and that the government should be the managers of those IDs.

“Private companies should not own that. It is the social contract of a citizen with their country to have an identity, a currency and safety. You should not take that away from them. They should have the digital identity. That digital identity should guarantee the privacy of that citizen. It should help them with their security, but the government should give the identity.

“Once you do that, then connecting them to the infrastructure that a private company, whether Ericsson or Verizon or combinations of them, in fact, mostly it’s a combination, can build.

“Then the question is, what do you do with it that requires that digital ID so you can start connecting with that citizen? Now the question is, when you connect with that citizen, you must ensure that governments guarantee the privacy of that citizen, because if you don’t do that, you will run into trouble with the acceptance of the idea. If you want this to be embraced around the world, yes, get the infrastructure, get a digital ID. That’s what we used to talk about even earlier. Get that going and then move from there.”

He went on to add:

“A sense of crisis is your best friend. Never let a crisis go waste. A sense of crisis is your best friend in getting people to agree to tackle this triangle, along with the enabling tool of technology and the biggest headroom is geopolitics and fractionizing of the global order. That’s why I believe in digital for us.”

On February 26th, the World Bank published a paper called “ID Meets Instant.”

The group wrote in a blog post summarizing its paper. The World Bank wrote (emphasis mine):

Imagine this situation - María runs a small grocery shop, and one afternoon she receives a message asking her to pay a supplier urgently through the country’s fast payment system. The name looks familiar. The payment request looks real. She sends the money. Minutes later, she realizes it was a scam. The money is gone.

Fast payment systems are incredibly powerful. They move money instantly, around the clock, at low cost. But speed also removes the margin for error. Once funds move, they are hard to recover. And today, many fast payment systems still rely on fragmented identity checks and app-specific controls that leave users exposed to fraud, misdirected payments, and unnecessary friction. This is where digital identity can fundamentally change the experience.

Beyond individual safety and convenience, the integration of fast payments and digital identity also helps create jobs and improve people’s lives. By reducing payment frictions, fraud risk, and onboarding barriers, these systems help small firms operate formally, get paid reliably, and scale their activities, while enabling workers and microentrepreneurs to participate more fully in the digital economy. In this way, trusted digital payments infrastructure directly supports job creation, productivity, and resilience.

Using Digital ID to Improve the Fast Payments Experience

In most countries, digital ID is used mainly at onboarding. You show your ID, open an account, and then identity disappears from the payment journey. Payments themselves rely on aliases, account numbers, or phone numbers, with limited ability for users to verify who they are really paying.

What if identity stayed with the transaction? In María’s case, the payment request could have carried a verifiable proof of the supplier’s identity, issued by a trusted authority and recognized across the payment ecosystem. Before sending the money, María’s phone could have shown: Verified merchant. Registered business. Credential issued by the national ID framework. If the identity did not match, the payment would trigger a clear warning.

This is not about adding new steps or slowing payments. It is about making trust portable and reusable, so that users can confirm who they are dealing with instantly, without friction.

The same approach improves other moments that matter: opening a new account in minutes instead of days, authenticating securely without juggling passwords or SMS codes, and sharing payment history safely to access credit or insurance without exposing raw data.

What It Takes to Make This Work

Importantly, this does not require new payment rails or a single national wallet. The approach explored in ID Meets Instant builds on existing fast payment systems and digital ID investments by introducing a portable Payments Identity Credential, that leverages verifiable credentials and is built on top of a trust framework established between National ID Authorities and operators and regulators of Fast Payment Systems.

The Payments Identity Credential can be understood as a portable digital portfolio for financial services—functionally similar to a card credential, but designed for open, account-based systems and capable of operating across multiple providers and providing access to various services and functionalities. It can bundle credentials issued by multiple banks and payment service providers into a single, reusable construct, enabling interoperability across the ecosystem while preserving user choice.

By carrying a KYC verifiable credential anchored in authoritative digital ID systems, the Payments Identity Credential supports instant onboarding across providers and reduces the risk of mule accounts and synthetic identities that exploit fragmented onboarding practices. During transactions, a verifiable presentation of the payee’s identity can be embedded in a QR code or request-to-pay message, allowing users to cryptographically validate the identity of a merchant or recipient before authorizing a payment.

The Payments Identity Credential also enables trusted, consent-based data sharing and authentication. Payment transactions and related information can be bundled into verifiable credentials within the Payments Identity Credential and selectively shared to support access to credit, risk assessment, and fraud prevention without exposing raw data. Authentication credentials embedded in the Payments Identity Credential can be reused across providers and channels in a manner analogous to other payment instruments, reducing user friction while strengthening security.

At a practical level, this means three things. First, identity becomes a credential that can travel. Instead of each bank or wallet redoing checks in isolation, trusted credentials can be issued once and reused, with user consent.

Second, verification happens at the moment of payment, not just at onboarding. Payment requests, QR codes, or request-to-pay messages can carry cryptographic proof of who is requesting or receiving funds.

Third, users stay in control. Credentials live in wallets or apps people already use. Only the minimum information needed for a specific transaction is shared, and permissions can be revoked.

Because this model operates as an overlay, countries can adopt it incrementally, starting with high-impact use cases such as confirmation of payee or instant onboarding.

Policy and Regulatory Safeguards Matter

Integrating identity more deeply into payments raises legitimate concerns. Who issues credentials? Who can verify them? What happens when something goes wrong? For this reason, the model emphasizes strong policy and regulatory foundations alongside technology.

A shared trust framework is essential, aligning digital ID authorities, payment system operators, and financial regulators. This framework defines how credentials are issued, validated, revoked, and supervised. It also clarifies liability and dispute resolution, which is critical in fast, irreversible payment environments.

Privacy and consumer protection are non-negotiable. Verifiable credentials support data minimization and consent by design. Users do not hand over full identity profiles; they present proofs. Regulators retain oversight, and competition is preserved by ensuring that no single provider controls access to credentials or wallets.

Finally, safeguards must anticipate what comes next. As fraud becomes more sophisticated and AI-driven agents begin to initiate payments on behalf of users, identity-based credentials provide a foundation for controlled delegation, auditability, and trust at scale.

Moving from Faster Payments to Better Payments

Fast payment systems have transformed how money moves. The next phase is about how safely, confidently, and inclusively people can use them.

By bringing digital identity into the heart of payment flows, countries can reduce fraud, simplify access, and make everyday transactions feel less risky and more efficient. The opportunity is not to build something entirely new, but to connect what already exists into a system that works better for users like María, every single day.

The World Bank’s blog post didn’t get into it, but digging into the actual paper itself, they do directly mention tokenization; and a lot of what they previously just described could or will involve tokenomics.

On page 14, discussing interoperability of digital IDs and Payment Identity Credentials (PIC), the authors write:

Credentials have long been familiar form factors in payments, whether through debit and credit cards, mobile money wallets, or app-based payment services. Because users and providers are already accustomed to credentials, extending these models to include [Verifiable Credentials] VCs can create a seamless transition. Integrating VCs into FPS is therefore not disruptive, but evolutionary, building on existing habits and infrastructures while enhancing them with stronger trust, security, and interoperability.

VCs can also bring tokenization-level security to FPS–digital ID integration while avoiding lock-in and enabling broader interoperability across wallets, schemes, and use cases. A central value of VCs is their ability to provide the same security and privacy safeguards traditionally achieved through tokenization, but in a more open and flexible way. By leveraging selective disclosure and cryptographic proofs, VCs ensure that sensitive identifiers never need to be exposed in the transaction process. This allows them to function as secure, dynamic credentials that can authorize access to FPS rails without reliance on proprietary token formats.

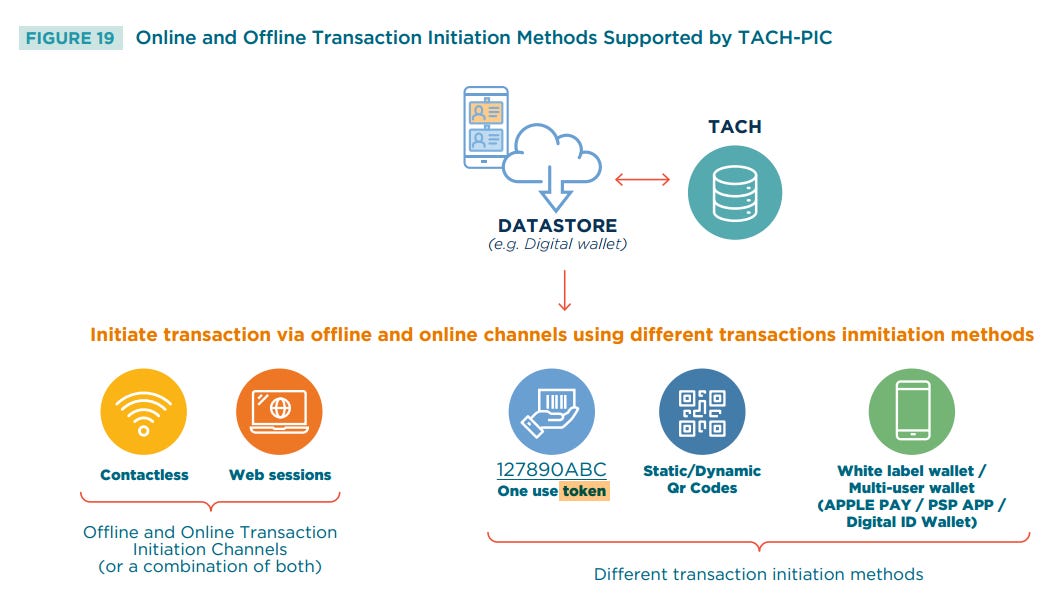

[…] Importantly, PICs are not tied to a single interface. They can be mobilized through contactless channels, web sessions, one-use tokens, or static and dynamic QR codes. They can also be linked to white-label wallets, multi-issuer wallets, or PSP-specific applications. This diversity of access channels and initiation methods ensures that PICs remain broadly usable, supporting inclusivity by meeting users where they are. At the same time, security is strengthened, since all PIC-based transactions are bound to VCs and initiated only after strong customer authentication. This dual focus on flexibility and assurance creates a credential that is both practical and trustworthy.

In other words, VCs can on-board tokenization but they are not dependent upon it either, allowing for interoperable systems that can work seamlessly together.

VCs will also enable tokenized government and merchant payments, the paper explains.

As for how this would work on an everyday level, the World Bank explains:

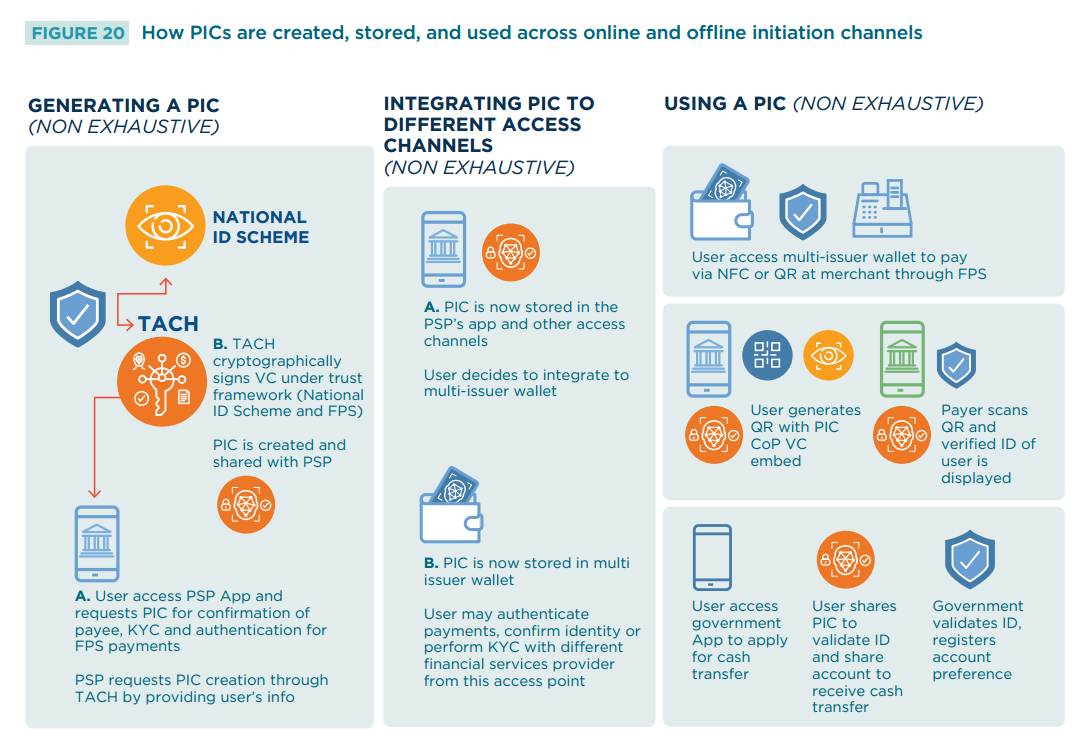

After storage, the PIC becomes part of everyday life. Users can authenticate payments, confirm their identity, or complete KYC processes with any connected financial service provider. This works across the following offline and online environments:

• At merchants: A user can tap their phone at a point-of-sale terminal using NFC, scan a QR code, or display a one-time token. The PIC ensures that payer and payee are verified instantly, reducing fraud.

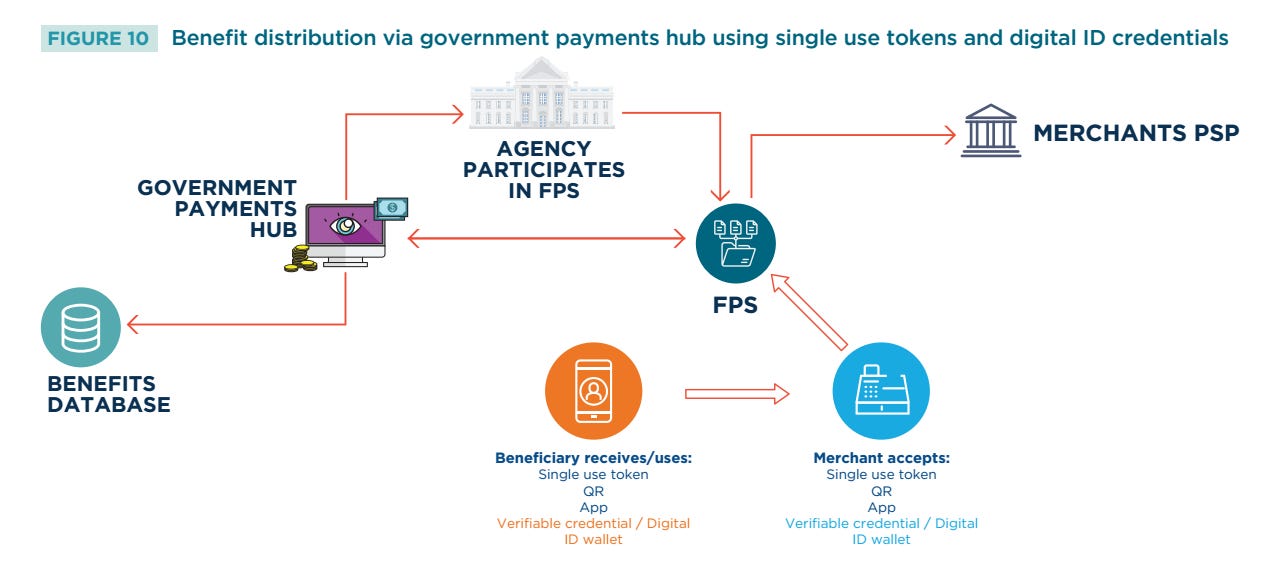

• In government services: A user can present their PIC when applying for a cash transfer. Their verified identity and preferred account are shared in real time, allowing the government to confirm eligibility and register payment details.

• In digital sessions: A user can rely on their PIC to log in securely through web sessions or to generate one-time codes for remote authentication, avoiding repeated credential entry. From the user’s perspective, these actions feel simple and familiar. They see prompts such as “Approve payment” or “Confirm identity.” The complexity of cryptographic verification, selective disclosure, and consent management remains hidden.

The authors note in their concluding and forward-looking thoughts that digital ID and tokenization will compromise the “new forms of money.”

New forms of money: As central banks explore digital currencies and as crypto and tokenized assets continue to grow, VCs can play a vital role in ensuring financial integrity. Tiered or purpose-bound credentials could enable compliant onboarding, transaction screening, and auditability without sacrificing usability. Explicit recognition of credentials across jurisdictions could also support cross-border experiments with central bank digital currencies and the integration of digital assets into regulated financial ecosystems.

AUTHOR COMMENTARY

What the World Bank did not say in its blog post is that instant transfer payment rails can also support the use of CBDCs and tokenization. A number of Federal Reserve officials have admitted this, as I pointed out last year when Trump (alongside Elon Musk) signed executive orders to modernize payment systems at the Treasury, and the EOs explicitly mentioned the use of instant transfer payment rails (FedNow), which opens the doorway for CBDCs (stablecoins in America’s case) and tokenization.

What the World Bank described is already occurring in India. Almost every single person will have a digital ID that is affixed to their instant transfer payment rail. This was discussed in joint talks with the World Bank and the International Monetary Fund (IMF) last year. India’s digital ID has proven so effective that there have been talks about whether the country should tokenize on a public scale. I think they eventually will, but it goes to highlight just how important digital ID is.

One of the speakers during one of the panel discussions was an Indian who works at the Bank for International Settlements, and he joked that people’s entire identities will be tokenized in just a number of years.

What the World Bank is saying is nothing new in of itself: we’ve heard BlackRock, the UN, the BIS, the IMF, and private institutions say something indentical about digital IDs. Digital ID is tantamount to their globalist and central banking objectives. With it, tokenization and the global social credit score surveillance state, where everything is eventually tracked, traced and programmed in real-time on blockchain ledgers is enabled. I’ve written about this extensively. Fink and others have made it clear that Digital ID must be in place for full-tokenization work.

I have had some people ask me how tokenization will work globally because so many countries, central banks and private corporate interests all have their own unique interests and platforms. Key word: INTEROPERABILITY. The World Bank explained that in this report. Digital ID, PICs and VCs, allow for central banks, treasuries, fintechs, Tradfi, instant payments rails to all work together because they know who you are. Therefore, in theory, fiat can be converted into conventional digital bank money (DBC) — what we have now — and that can be converted into stablecoin payments or CBDCs, whether it’s with private digital tokenized wallets (i.e. Coinbase, Kraken, Robinhood), or a say digital Yuan in China issued by the central bank, or if it is digital numbers on a screen in a non-tokenized economy like in India. The point is, all of it can then be reconverted seamlessly. That’s how you can have a public-private system (fascism) in the U.S., or CBDC only (communism) in China or parts of Africa, for example.

This is why I continue to harp on about this stuff. Digital ID is already here in the form of online transactions and search history: now it’s about consolidating that and enforcing that slowly overtime.

Why do you suppose Trump, for example, is working directly with Palantir and Oracle to combine all of our most personal and intrinsic data and genomic information about us? It’s the perfect system where they can eventually play God and “pondereth all [our] goings” (Proverbs 5:21).

Eventually, in the not-too-distant future, this will all be consolidated into the mark of the beast system. Tokenization lays the next bricks in the road to that goal.

Revelation 13:16 And he causeth all, both small and great, rich and poor, free and bond, to receive a mark in their right hand, or in their foreheads: [17] And that no man might buy or sell, save he that had the mark, or the name of the beast, or the number of his name. [18] Here is wisdom. Let him that hath understanding count the number of the beast: for it is the number of a man; and his number is Six hundred threescore and six.

The Lord Of Glory: The Detailed Guide To Who God Is – Available Now!

On one of his missionary journeys, the apostle Paul visited Athens, Greece, where he said he witnessed “the city wholly given to idolatry,” and who were “too superstitious” and worshipped a plurality of gods and deities, though the people acknowledged that there was still one God above all that was a mystery to them. When questioned by the philosophers …

[7] Who goeth a warfare any time at his own charges? who planteth a vineyard, and eateth not of the fruit thereof? or who feedeth a flock, and eateth not of the milk of the flock? [8] Say I these things as a man? or saith not the law the same also? [9] For it is written in the law of Moses, Thou shalt not muzzle the mouth of the ox that treadeth out the corn. Doth God take care for oxen? [10] Or saith he it altogether for our sakes? For our sakes, no doubt, this is written: that he that ploweth should plow in hope; and that he that thresheth in hope should be partaker of his hope. (1 Corinthians 9:7-10).

The WinePress needs your support! If God has laid it on your heart to want to contribute, please prayerfully consider donating to this ministry. If you cannot gift a monetary donation, then please donate your fervent prayers to keep this ministry going! Thank you and may God bless you.

I will be talking about the Iran situation soon.

For whosoever will save his life shall lose it: and whosoever will lose his life for my sake shall find it.

Matthew 16:25